What if I told you that the loose change slipping into your couch cushions could make you a millionaire by the time you retire? The trick? Swap out lottery tickets for investments and let the magic of compound interest do the heavy lifting. Here’s a look at how even a variable savings habit—sometimes $5 a day, other times $10—can secure your future in a way that no lottery ticket can.

Let’s meet Loose-Change Linda and Smart-Change Sam to see the difference between gambling on a “maybe” and investing in a “nearly guaranteed” jackpot.

Pocket Change for the Win: Lottery Tickets vs. Investing

Loose-Change Linda’s Lottery Gambit

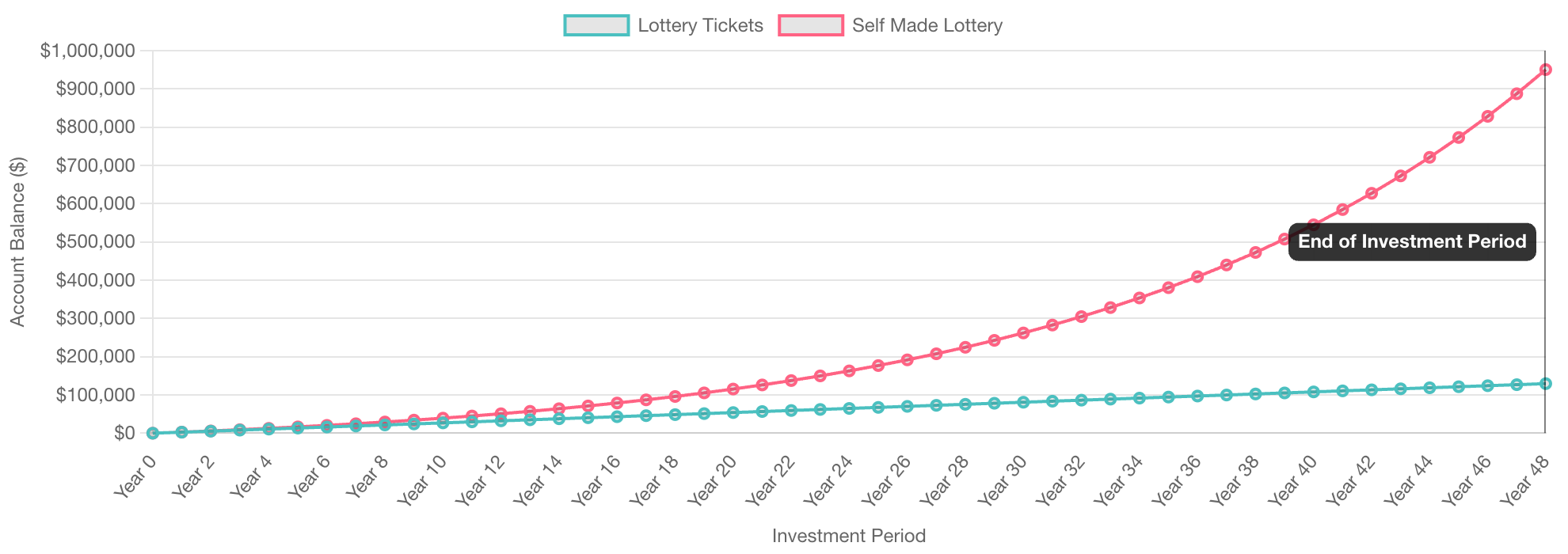

Linda has a dream: hit the lottery and retire a millionaire. So, she buys lottery tickets every day. Sometimes she’ll spend $5, other times $10, depending on how much change she digs up in the couch cushions or happens to have on hand. Over time, she spends about $7.50 a day on average, which adds up fast. In one year, she spends about $2,750, and over 47 years (from age 18 to 65), Linda burns through more than $128,000 on tickets. The return? A few small wins, but nothing close to life-changing.

Smart-Change Sam’s Investment Strategy

Sam has a different idea. Instead of spending his loose change on lottery tickets, he’s changing his mindset. When he finds an extra $5 or $10, he drops it into a low-cost index fund instead of gambling it away. Over the years, his daily average investment of $7.50 grows and compounds at an average return of 7% annually. By the time he’s 65, his sporadic $5-and-$10 contributions have ballooned to around $1 million. And it’s sitting in a retirement account, ready to support him in his golden years.

The Power of Consistency and Compound Interest

Sam’s million-dollar retirement didn’t happen because he saved $128,000 over time. It happened because of compound interest—letting his investment grow on itself, year after year.

- 10 Years In: Sam’s contributions total around $27,375, but compounding has boosted his investment value to about $38,200.

- 20 Years In: His $54,750 in contributions has grown to $112,000.

- 30 Years In: With a total contribution of $82,125, his investment has skyrocketed to $270,000.

- 47 Years In: By retirement at age 65, Sam’s investment has compounded to around $1 million – thanks to his habit of stashing just a few bucks here and there.

Changing the Game by Changing Your Mindset

Sam’s journey to a millionaire mindset started with a single decision: to invest, not gamble. Instead of throwing his change at a one-in-a-million chance, he put it into something that almost guarantees growth. And it didn’t even require strict discipline! Some days it was $5, some days $10—but it added up and compounded over time.

And the best part? This kind of saving can fit right into any lifestyle, no matter how tight your budget is. You don’t have to think of it as strict “saving.” Instead, treat it as a kind of financial “lost and found.” Every time you skip the lottery or stash some found change, you’re building your “Sure Win” account, a little at a time.

Smart-Change Sam’s Secret: The Real “Millionaire’s Lottery”

Saving and investing isn’t flashy, and it doesn’t offer the thrill of scratch cards or quick wins. But here’s what it does give you: peace of mind, a reliable path to financial independence, and the power to know you’re building wealth that will actually be there when you need it.

If you start young—say, at 18, like Sam—and put away an average of $7.50 a day, you’re setting yourself up for a real jackpot. It might not feel as exciting as winning the lottery, but that’s because it’s better. You’re guaranteed to come out ahead.

But wait! $1 Million Won’t Be as Much That Far Into the Future!

You’re right to think about inflation, but the calculations are in today’s dollars. For simplicity, we’re working with today’s purchasing power and not adjusting for inflation—or the extra lottery tickets inflation would have you buying. But here’s the thing: $1 million in investments is designed to grow with the market, typically outpacing inflation over time. So, even though $1 million decades from now might “feel” different, its relative value in securing your future is just as powerful. Nice try, though!

Final Thought: Turn the “Lottery” into Your Everyday Mindset

Next time you dig up $5 or $10 in the couch cushions or feel the itch to grab a lottery ticket, imagine that money in your future self’s hands. With a little patience, the change you stash now could turn into a secure, comfortable retirement. It’s like a daily lottery where you’re not just hoping for the win—you’re creating it, one day at a time.

Are you ready to start playing the millionaire’s “Sure Win” lottery? Give it a try today—and thank yourself at 65!